The trend of newer companies tapping the bond market to raise funds directly from retail investors has been a prominent development over the past year. Interest rates are peaking globally, and yields have stabilised after surging to record levels. The Reserve Bank of India (RBI) and the US Federal Reserve have hit the pause button for a while now.

It may be a good time for investors in fixed-income instruments to make the most of the present high interest rates and coupons.

NBFCs (non-banking finance companies) are coming out with non-convertible debentures (NCDs) with fairly high coupons and yields in recent months. The key advantage in such offerings is the attractive yield in the 2-3-year window, which is not otherwise easily available for retail investors.

360 One Prime (IIFL Wealth Prime earlier) has come out with an NCD offer that is opening for subscription on January 11. The company predominantly provides loans against shares to clients of the parent’s wealth management business.

The issue is rated AA (Stable) by CRISIL and ICRA. These ratings indicate a high degree of safety in servicing principal and interest, and very low credit risk. This NCD comes in four tenors with periodic interest payout options. The coupons are fairly attractive.

Here’s more on 360 One Prime’s NCD offer to help you take an informed investment call.

Playing the yields

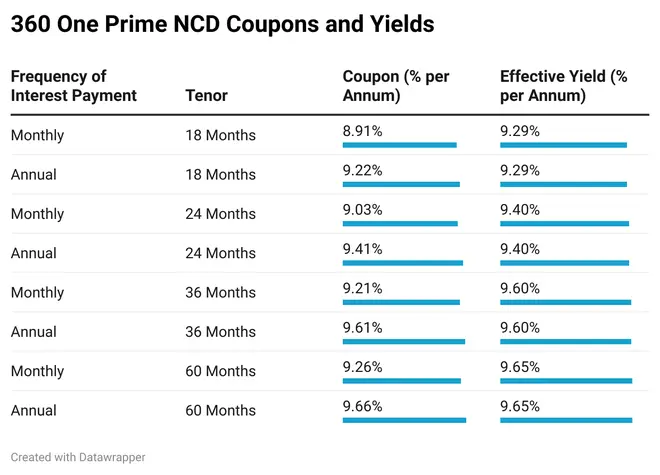

As mentioned earlier, the company’s NCD offer comes in four tenors – 18 months, 24 months, 36 months and 60 months. For each of these tenors, there are monthly and annual interest payout options for investors. There is no cumulative option.

360 One Prime offers coupons in the range of 8.91 per cent to 9.66 per cent across the four tenors and interest payout options. The effective yields on the various options range from 9.29 per cent to 9.65 per cent. Though not comparable, these coupons are much higher than the interest rate offered by most banks and NBFCs on their fixed deposits for similar tenors.

Data from Axis Bank (sourced from ICRA Analytics) as of January 10 indicate that corporate bonds rated AA with three-year tenor trade at 8.47 per cent yield on an average presently, while the yield on 5-year bonds is 8.37 per cent. On one-year corporate bonds, the yield is 8 per cent.

360 One Prime’s NCDs with three-year tenor are available at 9.6 per cent yield for monthly and annual interest payout options, a good 113 basis points more than what is available in the corporate bond market. The two-year and 18-month tenor NCDs with 9.4 per cent and 9.29 per cent yields, respectively are also quite healthy.

The minimum investment required is ₹10,000.

Investors can consider the 18-month, two and three-year tenors with monthly interest payout option so that the lock-in is relatively short and cash flows in the form of coupon payments are regular.

From April 1, 2023, tax is deducted at source on coupon payments in NCDs. In any case, all interest payouts are taxed at your slab.

Take modest exposure

360 One Prime (originally Chephis Capital Markets before being acquired in 2016) is a subsidiary of 360 One.

Now, 360 One Prime provides loans against securities (LAS) to its parent’s clients in the wealth management business. The LAS business accounts for 81.3 per cent of its loan book as of the first half of FY24. Loan against property (7.5 per cent of loan book) and unsecured lending (11.2 per cent) are the other lending segments.

- Total assets under management increased from ₹3,933 crore in FY22 to ₹4,927 crore in FY23 (AUM in H1 FY24: ₹4,848 crore)

- Borrowing cost fell from 7.37 per cent in FY22 to 7.5 per cent in FY23

- Yield in loans increased from 10.83 per cent in FY22 to 11.39 per cent in FY23

- Capital adequacy was at a healthy 24.03 per cent in H1 FY24 versus 19.78 per cent as of FY23

- The gross non-performing assets ratio (gross stage 3) were nil in all years of its operations, indicating reasonable asset quality

360 One Prime has a LTV (loan-to-value) of just 33.17 per cent in its LAS business and 37.14 per cent in its loan against property segment, giving it a fair margin of safety.

Given that the mainstay is the LAS business, 360 One Prime’s lending is subject to the ebb and flow of market movements, making it a tad risky.

However, given that the company’s metrics are reasonable and the parent company is well-established, investors can consider parking small sums in the NCD offer.

In general, NCDs must not account for more than 5-10 per cent of your debt portfolio.

The 360 One Prime NCD offer seeks to raise ₹200 crore, with the option to retain another ₹800 crore of oversubscription.

![]() Comments

Comments