For investors who wish to play the infrastructure theme, given the growing and significant focus of government on infrastructure development, Ircon International (Ministry of Railways undertaking) can be a good option. Budget 2023 has maintained the thrust on capex spending with ₹2.4 lakh crore on Railways and ₹2.7 lakh crore on road infrastructure. This is positive for Ircon International (Ircon) as the company is involved in infrastructure construction projects of roads, bridges, highways and railways in addition to other related works.

The company is trading at a trailing PE of 6.9x while other companies in the infrastructure sector, such as IRB infrastructure Developers, PNC Infratech, Rail Vikas Nigam Ltd, KNR Constructions and L&T are trading at a trailing PE of 25x, 12x,11.x,14.x and 30x respectively. The cheaper valuation, large orderbook, strong cash position and business prospects make Ircon an attractive buy option at current levels.

Business and prospects

Ircon is a government company with majority stake owned by Ministry of Railways (73.2 per cent) and is involved in major infrastructure projects. The company has very diversified expertise that encompasses roads, bridges, highways and railways, electrification, construction of buildings, station building, coach manufacturing, etc.

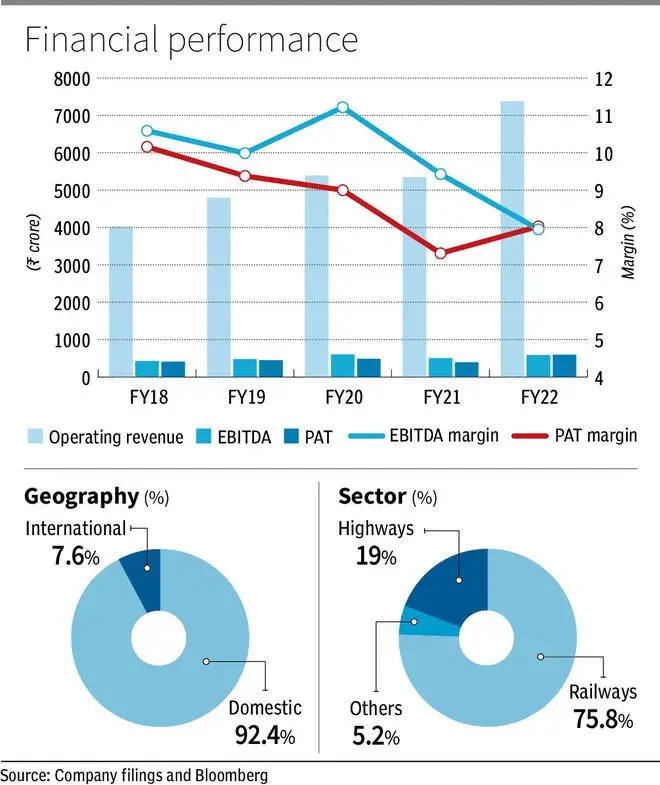

The company gets a major chunk of its projects from Railways, which accounted for 75.8 per cent of its order book as on December 31, 2022, at ₹28,834 crore. The company takes up various jobs for Railways, e.g., railway lines, bridges, tunnels, signalling and communication and electrification.

Ircon also has 19 per cent of order book from highway projects as on December 31, 2022, translating to ₹7,220 crore. The company is involved in development and maintenance of road assets and operates on BOT (build, operate and transfer), toll and annuity model, EPC (engineering, procurement and construction) or on Hybrid annuity model (HAM).

The company has both domestic and international businesses. The domestic business accounts for 92.4 per cent of the order book while international business makes up 7.6 per cent. Ircon takes up projects in countries such as Indonesia, Myanmar, Sri Lanka and Malaysia. Overall 50.1 per cent orders were achieved through nomination i.e., orders given to the company without the bidding process. Being a PSU, Ircon seems to have the advantage of getting projects on nomination basis from various government bodies e.g., it got a road construction project in Myanmar through Ministry of External Affairs for which the work is under process. Projects won on outright bidding make up 49.9 per cent of orderbook.

In December 2022 quarter, domestic revenue was 96 per cent of operating revenue while that of international was 4 per cent. The share of international revenue is expected to grow in coming times as it accounts for 7.6 per cent of orderbook.

Ircon has completed a project of setting up a coach factory in Raebareily worth ₹ 2618.07 crore and is presently involved in the construction of Mumbai Ahmedabad High Speed Rail Project (Package MAHSR C-7 & T-12) worth ₹ 1714.23 crore and ₹ 5143 crore. In recent times the company has bagged two projects. One is the railway project in Sri Lanka which will involve procurement of Design, Installation, Testing, Commissioning and Certifying of Signalling and Telecommunication system. The second is a Detailed Engineering and Project Management Consultancy (PMC) for Mahanadi coalfields Orissa worth.

Orderbook and guidance

The company has a total orderbook of ₹38,023 crore as on September 30, 2022, and considering FY22 revenue of ₹7379 crore, the book to bill ratio comes to 5.4, which means the revenue visibility of the company is close to five years. However, the management is of the opinion that this orderbook can be executed in 3-4 years.

The management has given revenue guidance for FY23 at ₹9,000-₹9,500 crore — from ₹7,379.67 crore in FY22. The company has stated that it intends to maintain net profit margin around 7.5 per cent. The management intends to bid for projects where the margins can be managed and is not interested in going for aggressive bidding at lower levels where margins cannot be maintained. The company has said that even for cost plus projects it is placing bids as cost plus 8-9 per cent margins.

Financials

In Q3 FY23, the company reported revenue of ₹2421.91 crore, which is a 33 per cent growth YoY. Core EBITDA in Q3 FY23 was ₹ 157.75 crore, which is 5.05 per cent lower YoY and the Core EBITDA margin de-grew to 6.7 per cent in Q3FY23 from 9.43 per cent for the same period the previous year. The management stated that in the current quarter it had to take one-off adjustment in the books of subsidiary on account of change in depreciation policy. The net profit for December 2022 quarter was ₹190 crore, which is a 40.19 per cent rise year on year.

Investment thesis

The stock has a strong set of financials with good revenue and growing EBITDA. The company also has a very strong balance sheet with a high net cash balance. It has net cash of ₹4,299.69 crore which represents 82.5 per cent of its current market cap. . The trailing PE is 6.9x which is cheapest among its peers. The Enterprise value is ₹1,152.17 crore, and the EV/Free cash flow (FY22 figure) amounts to 0. 79x. The EV/EBITDA of the company is very attractive currently at 1.22x.

The company has said that it will follow the DPE (Department of Public enterprises) guidelines for paying dividend i.e., the dividend will be the higher of 30 per cent of PAT or 5 per cent of net worth. The trailing dividend yield of the company is 4.5 per cent. Therefore, investors may buy the stock at current levels as this would enable investors to have exposure to the ongoing infrastructure theme and also on account of the company’s attractive valuations and decent dividend yields. The risk-reward here looks favourable to the investor. In the case of Ircon, it appears that markets may have mispriced the asset resulting in cheap valuations as has happened to PSU stocks in the past, that later see significant re-rating over a period of time. In fact, many PSU stocks have already seen re-rating in CY22. Ircon appears to have more steam left.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.